Quiver News

The latest insights and financial news from Quiver Quantitative

THE QUIVER QUANT

EXECUTIVE SUMMARY

Sara Jacobs sold up to $2M in Qualcomm (QCOM) stock. She is the granddaughter of Qualcomm cofounder Irwin Jacobs. Her net worth: roughly $83M. These are her first trades since 2021. QCOM was near record highs.

In insider trading this week: two S&P Global (SPGI) CEOs bought over $2M combined, both first-ever purchases. Patrick Industries (PATK) saw five insiders pile in with $2.3M after LCII merger talks collapsed. Betterware's (BWMX) CEO bought ahead of a Tupperware acquisition catalyst.

POLITICS

Insider Trumps $750M Stock Portfolio

The 113-page OGE filing reveals 3,711 individual transactions between January and March 2026. The portfolio is heavily concentrated in Big Tech, with dozens of $1M+ purchases. Read the full OGE filing here.

Here are some of the largest trades:

INSIDER DATA

4 Insider Buys Worth Watching

THE EDITORIAL QUANT

This Sunday in The Editorial Quant: the full breakdown of President Trump's OGE Form 278-T. We dug through every page to map the sector bets, the biggest individual positions, what he sold vs. what he bought, and which trades overlap with active policy decisions. The portfolio tells a story the headlines missed.

Sunday: the sector-by-sector breakdown, which trades coincide with policy decisions, and what this portfolio reveals about presidential investing that no headline covered.

Want more stories like this in your inbox every week?

QUIVER DATA

Government Contracts

SOCIAL MEDIA ROUNDUP

WHAT QUIVER’S POSTING

@quiverquant UPDATE 📈 NOTE: $MRVL is up another 8% this morning. - - #quiverquant #stocks #congress

→ How GLP-1 Corporations are Fighting in DC for Market Share

If you’ve turned on your TV or scrolled social media recently, you are probably familiar with prescriptions like Wegovy, Ozempic, and Zepbound.

GLP-1 is a naturally occurring product in the gut working to regulate blood pressure and slow digestion, signaling fullness to the brain. But pharmaceutical companies have manufactured a synthetic drug to mimic the effects of GLP-1, called “GLP-1 agonists”, which have historically been used to treat chronic diseases like Type 2 diabetes.

In 2014, certain GLP-1 agonists were approved for weight management, and by the 2020s, drug companies released weekly injections (and now daily pills) with higher weight loss efficacy than their earlier counterparts, driving sales through the roof. Just between 2019 and 2023, the number of individuals without type 2 diabetes prescribed GLP-1 agonists reportedly increased 700%.

With increased knowledge and demand for GLP-1 agonists, corporations have been rushing to capitalize and profit off its popularity.

However, many companies face legal and practical challenges entering this market, due to hundreds of follow-on U.S. patents filed by early manufacturers of the drug. FDA approvals can also take months to years, and that happens before the drugs even hit the market.

Vying for dominance in this industry are Danish Novo Nordisk and American Elli Lilly & Co, which have both overcome significant legal hurdles. In this newsletter, we will be giving an overview of where each firm stands today and what they are doing to attempt to win over the public (and the government).

NVO and LLY dominate GLP-1 sector

NVO stock performance since 2024

While NVO certainly established itself at the forefront of the GLP-1 industry early on, LLY’s stock performance has recently soared above NVO, indicating the company’s success is outpacing its Danish competitor. LLY’s success has largely been attributed to better clinical results (e.g., greater weight loss) than NVO’s.

LLY stock performance since 2024

NVO's monopoly in the GLP-1 industry is facing increased competition as demand and supply grow. Now at the forefront of GLP-1 manufacturing, LLY has poured billions into manufacturing GLP-1 drugs, with nearly three-quarters of its 2025 revenue coming from diabetes treatments.

LLY revenue breakdown by sector

Lobbying spending goes up as patents face expiration

2025 saw some of the highest corporate lobbying counts in recent years, with LLY’s lobbying reaching over $10 million and NVO spending over $7M in lobbying.

Both companies’ lobbying efforts mirrored one another — With Trump implementing policies and Executive Orders aimed at capping the price of GLP-1 drugs for qualifying Medicare recipients, and new tariffs increasing prices of imports and exports worldwide, drug manufacturers reacted with increased corporate lobbying efforts and 2026 election donations.

Despite being based in Denmark, over half of NVO’s revenue is from North America, meaning its total profit is heavily influenced by American policies on drug pricing and access. So far in 2026, NVO has spent about $3.4m on lobbying for issues like IRA implementation, patent protection, and Most Favored Nation drug pricing (caps U.S. drug costs at global prices).

NVO revenue breakdown by geography

LLY has topped that at nearly $6 million spent on IP protection and market access within current trade negotiations. Essentially, increasing IP protections abroad prevents foreign drug companies from producing early generic copies of patented prescriptions like Foundayo or Zepbound.

LLY and NVO also made multiple donations to Republican candidates who have supported policies aimed at increasing patent and intellectual property protection, while opposing drug capping policies included in the Inflation Reduction Act, including Richard Hudson, Kevin Hern, and House Majority Leader Steve Scalise.

GLP-1 Industry could impact stocks from breath mints to packaged snacks

With patents set to expire, companies pouring research into biosimilars, and the introduction of new oral GLP-1 medications, drugs like Ozempic or Foundayo will become more and more accessible and affordable. J.P. Morgan estimates the industry will reach $200 billion by 2030, and the number of consumers of GLP-1 could more than double.

So as GLP-1’s continue to dominate the market and access to the prescriptions grows through programs like the

THE QUIVER QUANT

EXECUTIVE SUMMARY

New this week: We just launched ChatGPT Quiver Enhanced, our first AI-powered trading strategy. Every week, it analyzes Quiver's congressional trading, insider, and alternative datasets to pick 10 stocks with full AI justifications. See this week's picks below.

Two U.S. senators violated the STOCK Act this week. Sen. Rounds sat on a $1M-$5M stock sale for 208 days. Sen. Hickenlooper waited 351 days to disclose a Liberty Broadband sale. The STOCK Act gives them 45 days. Both chair subcommittees that directly oversee the industries they were trading.

Leopold Aschenbrenner, the ex-OpenAI researcher who wrote the famous AGI playbook, is expected to file his next 13F this week. His $5.5B fund made Bloom Energy its #1 bet at 22% of the portfolio last quarter. Bloom Energy has risen 65% in the last month. Full breakdown below, plus a link to track his portfolio live on Quiver.

In insider trading, Sportradar's CEO personally bought $10M of stock after Muddy Waters called 40% of revenue illegal. Six directors joined him. Sara Jacobs up 29.96% this week as QCOM hit all-time highs. Full breakdown below.

BUILDING QUIVER FOR YOU

Got 90 seconds? Tell us what features you want, report a bug, or let us know what is working. Every response gets read. Share your feedback here →

STRATEGY PERFORMANCE

POLITICS

Top Congress Portfolios This Week

POLITICS

Leopold Achenbrenner’s $5.5B Fund Files This week

QUIVER DATA

Significant Insider Purchases This Week

THE EDITORIAL QUANT

Two Senators on the Same Committee. One Bought. One Sold. The Trade? Constellation Energy.

This week in The Editorial Quant: Sen. John Boozman (R-AR) bought Constellation Energy on April 2. Sen. Shelley Moore Capito's spouse sold it on April 17. Both sit on the Senate Environment and Public Works Committee, which directly regulates nuclear energy policy and environmental permitting. Capito chairs the committee. CEG is the largest U.S. nuclear fleet operator and one of the cleanest plays on AI data center power demand. Two members of the same committee, opposite reads, same stock, same two-week window. We pulled the data.

This weekend: the historical pattern when consumer sentiment and market prices diverge this sharply, what insider and congressional trading signals tell us, and whether the smart money is positioning for a correction or acceleration.

Want more stories like this in your inbox every week?

SOCIAL MEDIA ROUNDUP

WHAT QUIVER’S POSTING

@quiverquant CONGRESS TRADE ALERT 🚨🚨 #quiverquant #congress #stocks #investing #breaking

THE QUIVER QUANT

EXECUTIVE SUMMARY

OpenAI missed its revenue and user targets last week according to the Wall Street Journal, sending Oracle down 4% and SoftBank down 10%. The report landed the day before Meta, Amazon, Alphabet, and Microsoft all report Q1 earnings. The question now is whether $600B in committed compute contracts gets honored.

On the congressional side, Rep. Salazar disclosed 20+ stock purchases after going 12 months without a single trade, including Corning (GLW) bought 12 days before Meta broke ground on a $6B fiber-optic manufacturing expansion. She sits on the House Financial Services Committee. Full trade list in the alert below.

In insider trading, Everforth's CEO bought $1M worth of stock on rebrand day and 15 other insiders bought alongside him. Charter directors bought $2.37M the same day Wells Fargo cut their price target. X-Energy directors bought shares at IPO price after the stock already ran 56%. Sara Jacobs up 17.70% this week

Full breakdown below.

BUILDING QUIVER FOR YOU

Got 90 seconds? Tell us what features you want, report a bug, or let us know what is working. Every response gets read. Share your feedback here →

POLITICS

Top Congress Portfolios This Week

QUIVER DATA

Significant Insider Purchases This Week

THE EDITORIAL QUANT

The Sentiment Paradox of April 2026

This Thursday. The S&P 500 closed at an all-time high of 7,165. Nvidia crossed $5 trillion. Intel posted the biggest earnings beat of the quarter. And yet consumer sentiment just hit 49.8, the lowest in the University of Michigan survey's 74-year history. Inflation expectations surged to 4.7%. We dig into what the data says when markets and consumers completely disagree, and what congressional and insider trading patterns look like during past sentiment divergences.

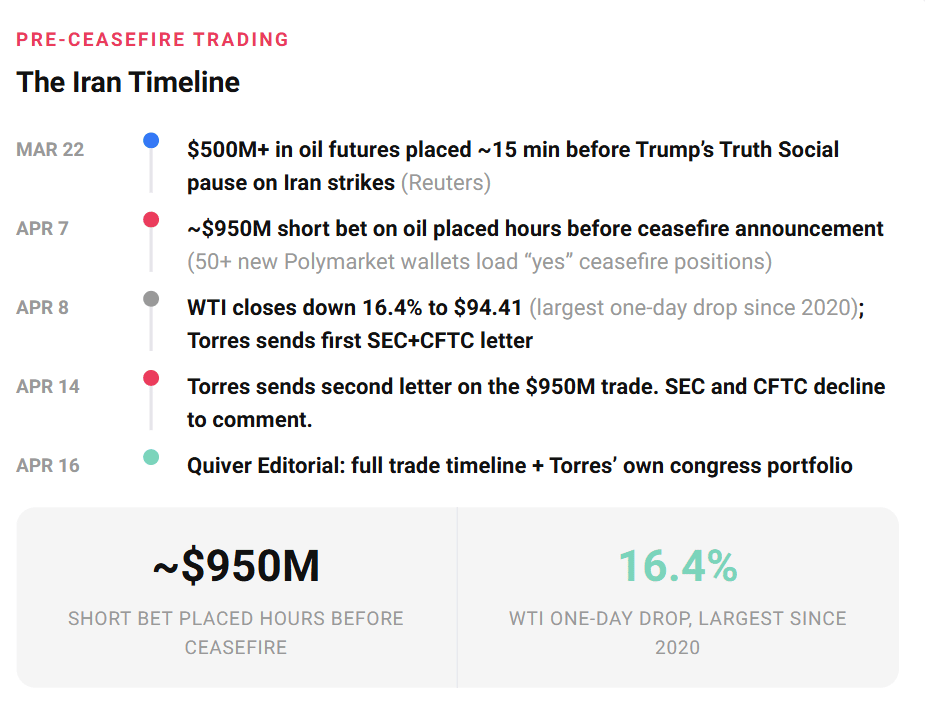

Also this Thursday: Who moved size before the announcement, what Torres’ own Quiver-tracked portfolio looks like, and whether this one actually gets enforced when the last two didn’t.

Want more stories like this in your inbox every week?